SELL IN MAY & GO AWAY? – A 50% PLUNGE IN U.S. STOCKS MAY BE IMMINENT, WARN EXPERTS

US stocks: is a 50% decline imminent?

Veteran hedge fund manager Jeremy Grantham also warned about the risk of a large and imminent market correction. Grantham notes an ongoing deterioration of financial conditions and believes that a crisis in the housing market could trigger the final phase of the financial bubble with the S&P 500 dropping to 3,200 by year end 2023. Grantham’s worst-case scenario would be a 50% decline to about 2,000, which could extend deep into 2024.

Stocks and the “Presidential cycle”

Perhaps the most interesting part of his analysis regards the timing of the correction: he expects that it will begin in May of this year and suggests that this is related to the “Presidential cycle.” Namely, the October through April period of a presidential administration’s 3rd year tends to be the most bullish period for stocks. According to Grantham, stock performance during those seven months have equalled the remaining 41 months in all presidential cycles – a pattern that’s held since 1932!

Here’s how he explains the phenomenon: every president wants a strong labor market in the 6-month run-up to the elections so that the voters feel favorable towards his administration and his party. Therefore, the administration seeks to stimulate the economy well in advance of the election cycle, since the impact of the stimulus only filters through to the labor market with a lag. Before that, the stimulus tends to have a more immediate impact in the stock market, which is why the seven months from October through April of the administration’s 3rd year tend to be the most bullish for stocks.

For the Biden administration, this seven month period will expire at the end of this month, which is why Grantham believes that the next leg of the downturn begins in May. Grantham adds the quip, “sell in May and go away…” Importantly, he warned that this might not be just a mild decline but rather an event comparable to 1929, 1973 or 2000. Today’s crisis is significantly worse than what we experienced in 2000 because it involves not just the stocks but also bonds and real estate, which is why Grantham is more inclined to expect his worst case, -50% scenario, reminding that in 2000 Nasdaq dropped by 82% and the S&P 500 by 50%.

Maybe they’re right. Or not?

There’s a 50% probability that Faber and Grantham are right (they either are or they aren’t) and I much prefer to remain agnostic about the future trajectory of security prices. History offers many examples where economic crises actually led to a sharp appreciation of asset prices. Where I do agree with both Faber and Grantham is that we will likely experience very significant price events in the markets, whether on the upside or otherwise.

Time to recovery

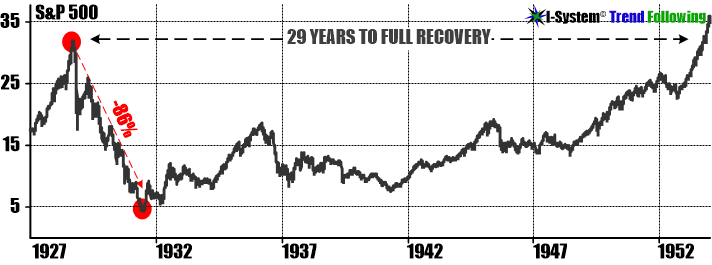

Another serious concern if Grantham’s and Faber’s predictions come to pass, is the time the markets will take to recover after such a strong correction. Over the last 40 years, even big corrections and/or bear markets recovered within a few years. But the real-deal, severe bear markets can take decades to recover as we saw in the aftermath of the 1929 crash:

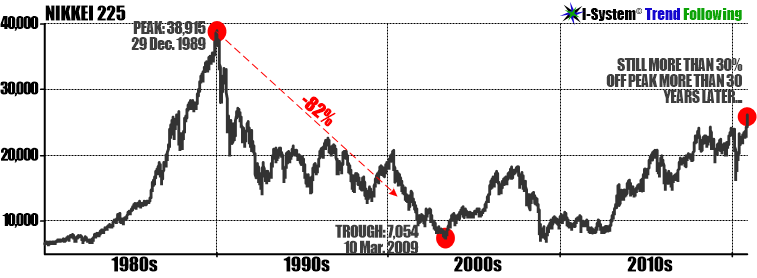

The Japanese stock market still never recovered after its 1980s bubble collapsed:

We can’t know what the future holds, but the range of possible outcomes today is very concerning.

Trend following beats prediction

Instead of guessing which prediction is wrong and which is right, investors will be better served by relying on systematic trend following strategies – at the very least as a source of second opinion about the unfolding trends. Trend following is the most reliable way to make sure you are on the right side of large-scale price events, whatever their direction.

The chart above illustrates the performance of a typical systematic trend following strategy during the 2008 financial crisis. Of course, the algorithm did not “know” to sell at the top nor buy at the bottom. But it also didn’t need to worry about predicting future events. Instead, it generated large windfalls during both bull and bear cycles by simply reacting to market trends as they unfolded.

For trend followers, even a bear market can be golden

Markets move in trends and trends can be advantageous even in a down cycle. Unburdened by convictions and opinions that might ultimately prove wrong, trend followers can profit during bull market cycles and during bear markets. As Sun Tzu knew more than 2000 years ago: there are three avenues of opportunity – events, conditions, and trends. For solutions, please see below.

Alex Krainer – @NakedHedgie is the creator of I-System Trend Following and publisher of daily TrendCompass reports which cover over 200 financial and commodities markets. For US investors, we propose a trend-driven inflation/recession resilient portfolio covering a basket of 30+ financial and commodities markets. For more information, you can drop me a comment or an email to xela.reniark@gmail.com – Originally published on Alex Krainer’s Substack. – ZERO HEDGE

Home Foreclosures And Missed Credit Card Payments Surge As Consumers Buckle

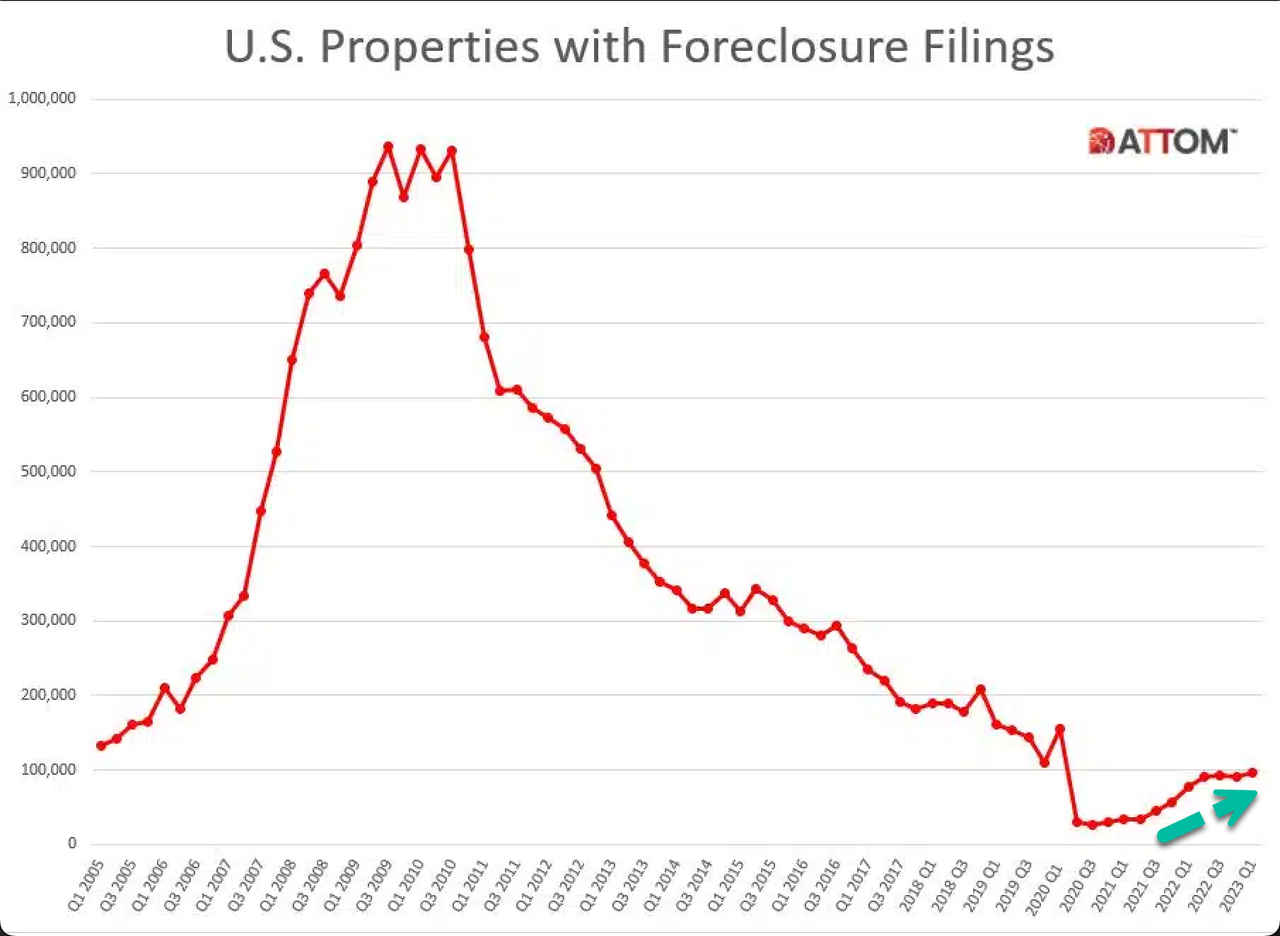

In the first quarter of this year, home foreclosures surged, as reported by property data firm Attom. Following a two-year lull, pandemic-related housing assistance programs are winding down. Homeowners who chose not to make mortgage payments are now either negotiating new terms with lenders, selling their properties, or, as current trends suggest, facing foreclosure. This troubling rise coincides with consumers falling behind on their credit card payments.

While still below pre-pandemic levels, foreclosure filings during the first quarter of 2023 totaled 95,712 properties, up 6% from the previous quarter and 22% from a year ago. This was the 23rd consecutive month with a year-over-year increase in foreclosure activity.

“This unfortunate trend can be attributed to a variety of factors, such as rising unemployment rates, foreclosure filings making their way through the pipeline after two years of government intervention, and other ongoing economic challenges. However, with many homeowners still having significant home equity, that may help in keeping increased levels of foreclosure activity at bay.”

Much of Attom’s data was recorded before Silicon Valley Bank’s demise. A credit crunch followed and sparked further busting of the tech bubble that added capital destruction in private equity and venture capital firms. Now real estate investments, primarily commercial real estate, are being significantly reevaluated as more financial stress is boiling up.

Making matters worse is 24 months of negative real wage growth for consumers who’ve maxed out credit cards and drained personal savings. Lower-tier consumers are coming under pressure as big banks are beginning to notice a startling uptrend in credit card and loan payment delinquencies.

“We’ve seen some consumer financial health trends gradually weakening from a year ago,” Wells Fargo Chief Financial Officer Mike Santomassimo said on an earnings call last Friday.

Banks have tightened their lending standards ahead of expected turmoil among consumers.

Wells Fargo set aside $1.2 billion in the first quarter to cover potential loan losses.

Bank of America provisioned $931 million for credit losses in the quarter, much higher than the $30 million a year prior but below the fourth quarter $1.1 billion provision.

JPMorgan more than doubled the amount it set aside for credit losses in the first quarter from a year earlier to $2.3 billion, reflecting net charge-offs of $1.1 billion. –Epoch Times

UBS analysts led by Erika Najarian believes mounting macroeconomic headwinds would lead to “credit deterioration throughout 2023 and 2024 with losses eventually surpassing pre-pandemic levels given an oncoming recession.”

Najarian said loan defaults are forecast to stay “below the peaks experienced in prior downturns.”

However, we’re noticing that consumers are buckling under financial pressure—an ominous sign of trouble ahead. ZH

ZERO HEDGE

.